NAIC regulators continue pushing for annuity illustration updates

State insurance regulators are seeking to reopen a key annuity illustration model regulation as they consider a significant overhaul of how illustrations are used in the sales process.

The National Association of Insurance Commissioners' Annuity Illustration Working Group held conference calls last week and this week in an attempt to forge a consensus path forward on the polarizing issue of illustrations.

Under Chairman Ben Slutsker, director of life actuarial valuation at the Minnesota Department of Commerce, regulators are weighing revisions addressing illustration length, disclosure requirements, accountability measures and how insurers present non-guaranteed crediting rates.

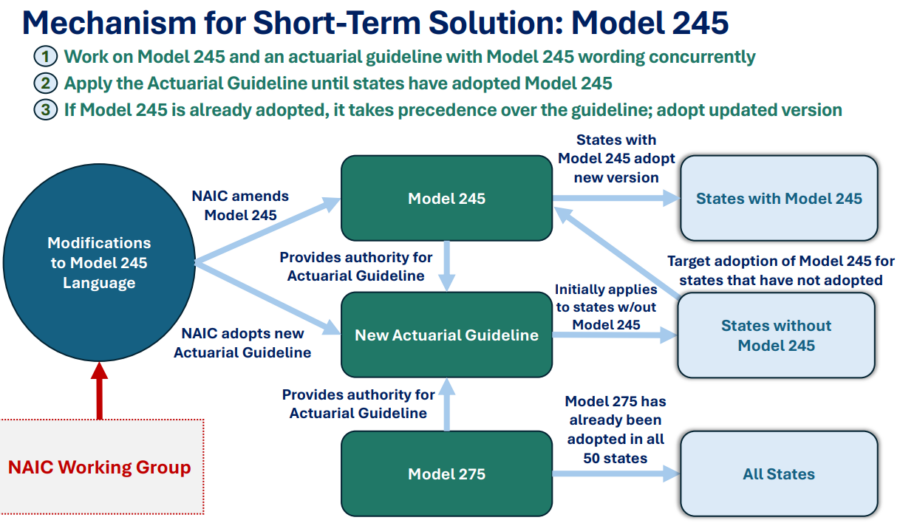

But first, the working group needs approval from its parent committee, the Life Insurance and Annuity Committee, as well as the NAIC Executive Committee before it can reopen the annuity illustration model #245.

"Hopefully, in the next couple of months we can get sign off there to reopen the model, at which point under NAIC policy I believe we have a year … to modify the model,” Slutsker explained.

The group is simultaneously considering a temporary "stopgap" approach through an actuarial guideline that could be used before any model revisions are adopted by individual states. Industry trade groups eyed that idea warily.

“We think that there are some other alternatives that you could use as a stopgap that is not an actuarial guideline,” said Carrie Haughawout, senior vice president of life insurance and regulatory policy at the American Council of Life Insurers. “There are some questions about whether an actuarial guideline is going to go beyond and act more like a policymaking tool than a guideline.”

Slutsker shared this flow chart plan for a stopgap solution:

'A lot of people don't understand'

Regulators spent much of Tuesday’s meeting discussing a list of potential modifications compiled from public comment letters. Several proposals focused on shortening annuity illustrations, which some regulators said have become overly lengthy and difficult for consumers to understand.

Joshua Blakey of the Oregon Division of Financial Regulation expressed support for combining multiple illustration scenarios into a single ledger, arguing that side-by-side comparisons could reduce consumer fatigue caused by lengthy documents.

Shorter illustrations would not only reduce document volume but also help consumers avoid being distracted by large projected account values generated through decades of compound growth, said Mike Yanacheak, chief actuary at the Iowa Insurance Division.

“A lot of people don't really get and understand compound interest and what it can do and might miss the whole point of what the illustration is trying to show about how a product works when it just dazzles with really, really big numbers that might be 50 or 70 or more years out," Yanacheak said.

Consumer advocates urged regulators to focus on simplifying disclosures rather than adding complexity.

Bonnie Burns of California Health Advocates said consumers often struggle to understand annuity products and may be unaware of fees and charges associated with riders and benefits.

She suggested a simple question-and-answer format addressing common consumer concerns, including benefit eligibility requirements, costs and long-term care features increasingly attached to annuity products.

And it is worth repeating some information contained in the Annuity Buyer’s Guide, Burns stressed.

“The buyer’s guide is a great tool,” she said, “but not everyone will read that, and they certainly won't read it at the time of sale. Some duplication of the most common things that consumers are concerned about would be an appropriate disclosure.”

Education or sales?

A significant portion of the discussion focused on how insurers should illustrate non-guaranteed crediting rates, one of the most contentious issues facing the working group.

Some participants questioned whether illustrations should be used primarily as educational tools or as sales tools that allow consumers to compare competing products.

Some speakers urged regulators not to eliminate consumers' ability to compare products from different insurers. Others argued that illustrations should focus on explaining product mechanics rather than projecting future performance.

Blakey said illustrations that function as sales tools create incentives for insurers to show increasingly optimistic crediting rates.

“I feel like the more that these are used as sales tools, the more incentive there is to show higher and higher crediting, regardless of the product type, if you're trying to differentiate yourself from competitors,” he said. “So, I like the idea of trying to make them more informational and educational than a sales tool.”

There are rate sheets and brochures and other items that can be used as advertising, Blakey added.

The working group plans to release two 45-day exposure drafts: one seeking feedback on potential modifications to Model 245 and another requesting comments on the proposed actuarial-guideline framework and alternative stopgap measures.

Regulators said they expect to review comments later this summer as they continue work on the model revision effort.

© Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Wisconsin releases enforcement actions for May

Why advisors should be talking about life settlements

Advisor News

- Amid slew of corporate tax ideas, Newsom chose one likely to hit people’s premiums

- The biggest risk to your clients’ financial plans isn’t market volatility

- Initiative looks at how caregiving impacts workplace benefits

- Will rising retirement needs spark an annuity boom?

- Living longer, retiring poorer: Why fragmented systems are failing Americans

More Advisor NewsAnnuity News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- Fortitude Re Completes $500 Million FABN Issuance

- Reframing retirement income for greater certainty

- Jackson Introduces Dow Jones Industrial Average Index Option, Flexible Premiums, Six-Year Rate Guarantee in Latest Registered Index-Linked Annuity Launch

- Senior Market Sales® Fortifies Annuity Reach With Acquisition of Retirement Planning Firm Stratton & Company

More Annuity NewsHealth/Employee Benefits News

- Health Care Notes: Clover star rating raised after court-ordered recalculation

- NORTH CAROLINA WOMAN CHARGED WITH CONSPIRACY TO COMMIT IMMIGRATION FRAUD, VA DISABILITY FRAUD

- Cigna tops Conn. Fortune 500

- ACA premium shock: Health insurers request hikes up to 30% for 2027

- More Hoosiers go uninsured, resulting in higher emergency department usage

More Health/Employee Benefits NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- Greg Lindberg moves to halt $1.65B restitution order, claims he ‘overpaid’

- Fidelity Investments® to Expand Target Date Lineup With Launch of Guaranteed Income Solution

- KBRA Releases Research – Private Credit: Much Ado About Nothing – Perspectives on Columbia Business School Paper About Private Ratings

- VUL sales skyrocket in Q1, signaling major market shift

More Life Insurance News